COVID-19 and Value: Impact Depends on How Long This Lasts

Loss of Rent and Property Value

In Seattle and across the country, temporary Covid-19 eviction moratoriums have led to numerous occupied, non-paying rental units. The uncertainty behind this new-normal is bound to have impacts on property values as rental income continues to fall. In order to understand the potential impacts, we must first comprehend how rental income, vacancies, cap rates, and values work together.

Vacancy Rates

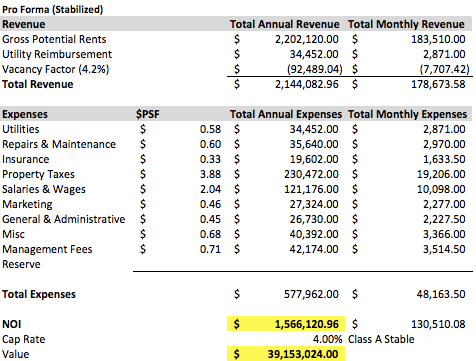

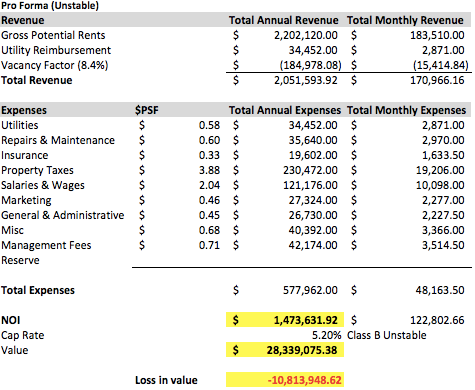

Per industry standards, a vacancy rate of 5% or less signifies a stabilized property (however, individual property owners may have their own standards for this). When units are physically occupied, but financially vacant, property owners face a higher vacancy rate, and thus significant rental income loss. The rate of occupied, non-paying units’ stacks on top of the property’s existing vacancy rate, often creating a vacancy rate above 5%, making the property unstable.

Cap Rates

Cap rates are used across the industry to signify a property’s risk level. Higher cap rates portray higher risk, but also higher returns. Conversely, lower cap rates signify low risk, with marginally lower returns. Cap rates vary for each property class. Class A properties are well-located, stabilized, newer properties, that yield lower cap rates. Class B properties may be older, not well located, or not quite as stable.

The problem with using cap rates to show property value loss during a pandemic or recession, is that cap rates do not typically move much during temporary events. Losses due to Covid-19 regulation, being temporary and shared across all property-levels, would not necessarily result in a cap rate moving upward.

The property generally stays in the same physical state, although the owner may defer maintenance projects until income is more certain. The main loss in rental income can lead to the property becoming unstable because of the increase in “vacancy.” At that point, an owner may consider a higher cap rate (unstable Class A cap rate properties may move to a conservative Class B rate to depict risk). However, the current crisis may be too temporary to assume any cap rate changes. If the Covid-19 regulations stick around for a significant amount of time, this may create a different story.

Values

The most prevalent place where rental income losses can be seen in a property’s financials, is in the actual monetary value of the property. There are many ways to derive value, but a simple way is simply dividing Net Operating Income (NOI) by the cap rate (owner derived or industry standard). Net Operating Income is determined by rental income, vacancy losses, and operating costs. When vacancy losses increase, rental income decreases. If the cap rate stays constant, but NOI is reduced, the monetary value of the property may significantly decline. Additional value losses can be seen if the property owner elects to use a higher cap rate.

Overall, rental income losses due to Covid-19 regulation will impact short-term property values. However, if the COVID-19 crisis remains temporary nature of this current crisis is not likely to yield long-term negative value effects.